If you’re an incorporated business owner in Canada paying for dental work, prescriptions, glasses, or therapy out of pocket, you’re likely leaving thousands of dollars in tax savings on the table every year.

A Private Health Services Plan (PHSP), commonly called a Health Spending Account (HSA), lets your corporation pay for your family’s medical expenses as a 100% tax-deductible business expense. You receive the benefit completely tax-free. No premiums. No deductibles. No copays. No insurance company deciding what’s covered.

It’s one of the most straightforward tax planning tools available to Canadian business owners. And yet, most of the clients we work with at Jones & Cosman have never heard of it until we bring it up.

This guide covers everything you need to know: how PHSPs work, who qualifies, what’s covered, how much you’ll actually save, and the critical mistakes that can trigger CRA problems.

What Is a Health Spending Account (HSA) in Canada?

A Health Spending Account is a CRA-approved arrangement that allows a Canadian corporation to reimburse its employees (including owner-employees) for eligible medical expenses. The reimbursement is a 100% tax-deductible expense for the corporation and a 100% tax-free benefit for the employee.

The formal CRA term is a Private Health Services Plan (PHSP), defined under section 118.2(2) of the Income Tax Act. You’ll also see it called a Health Care Spending Account (HCSA). These are all the same thing: different names used by different providers for the same CRA-approved structure.

Important note for Canadians searching “HSA”: A Canadian HSA is completely different from an American HSA. In the U.S., an HSA is a personal savings account with tax-advantaged contributions. In Canada, an HSA is an employer-funded plan where the corporation pays the expense directly. There is no personal contribution, no investment component, and no annual contribution limit in the American sense. If you’ve been reading U.S. financial content, reset your expectations. The Canadian version works differently.

The underlying mechanism is called the “cost plus” model. Your corporation pays the actual cost of the medical expense, plus a small administration fee to the HSA provider (typically 5-10%). That’s the entire cost. No monthly premiums, no per-person fees, no deductibles.

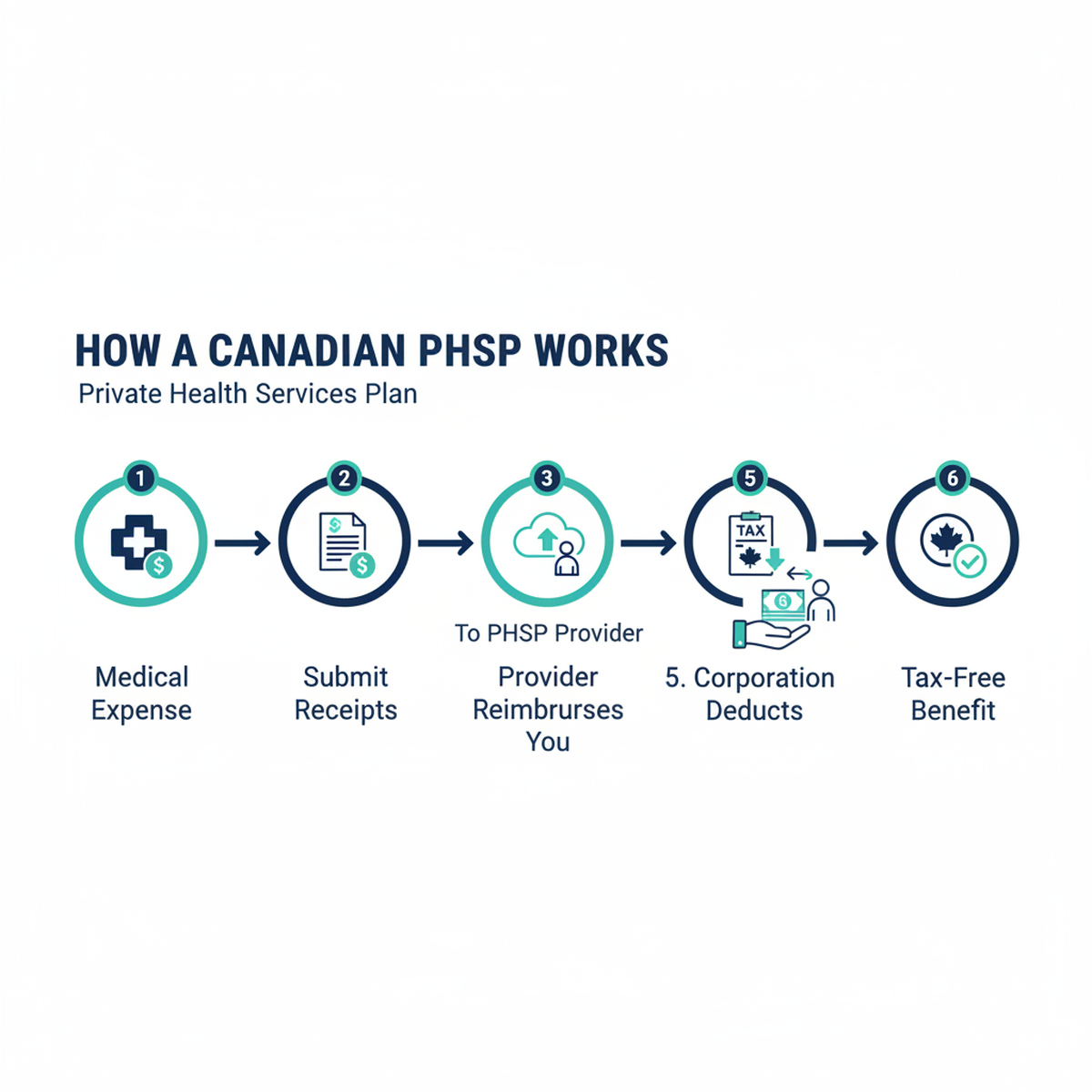

Here’s how the money flows:

- You or a family member incurs an eligible medical expense (dentist visit, prescription, therapy session)

- You pay out of pocket and get a receipt

- You submit the receipt to your HSA provider

- The provider reimburses you from your corporation’s account

- The corporation deducts the full amount (expense + admin fee) as a business expense

- You receive the reimbursement tax-free. It does not appear on your T4.

That’s it. No claims adjudication, no coverage limits set by an insurance company, no waiting periods for pre-existing conditions.

Who Can Set Up a Health Spending Account?

Not every business structure qualifies equally. The rules depend on whether you’re incorporated or operating as a sole proprietor, and how you pay yourself.

Incorporated Businesses (Including One-Person Corporations)

If you operate through a Canadian corporation, you have the most flexibility. Your corporation can establish a PHSP that covers you, your spouse, and your dependent children. This works even if you’re the only employee of your corporation.

The key requirement: you must be an employee of your corporation, not just a shareholder. This means you need to be on payroll and receiving T4 income.

This is where it gets important.

The Salary vs. Dividend Requirement (This Is Critical)

Many incorporated business owners pay themselves entirely through dividends because dividends avoid CPP contributions and can be more tax-efficient in certain brackets. That’s fine for general tax planning. But it creates a problem for PHSPs.

If you only pay yourself dividends and no salary, you are not technically an employee of your corporation. You’re a shareholder. And a PHSP is an employee benefit. If CRA reviews your file and sees a corporation claiming PHSP deductions for someone who receives zero T4 employment income, they can reclassify the entire benefit as a shareholder benefit under section 15(1) of the Income Tax Act. That means:

- The corporation loses the deduction

- You pay personal tax on the full amount of the medical expenses

- Penalties and interest may apply

This is exactly the scenario a client brought to us recently. They’d signed up for a PHSP through a provider, and the provider correctly flagged that they needed to maintain at least a modest salary to keep CRA comfortable.

The right salary amount depends on your specific situation: your province, your PHSP claim level, your overall compensation structure, and how CRA might view the relationship between your salary and your benefits. There’s no one-size-fits-all number. This is a conversation to have with your accountant, who can model the optimal amount based on your actual circumstances.

Keep in mind that salary means CPP contributions (both employee and employer portions), but it also builds CPP retirement benefits and RRSP contribution room. Your accountant can weigh all of these factors together.

Bottom line: If you’re currently dividend-only and want an HSA, you’ll need to keep your payroll account open and issue yourself a T4 each year. The appropriate salary level is a conversation to have with your tax advisor.

Sole Proprietors and Partnerships (Different Rules Apply)

If you’re not incorporated, the rules are more restrictive. A sole proprietor can only establish a PHSP if:

- You have at least one arm’s-length employee (not your spouse, not your child, not a family member unless they work for you in a legitimate capacity and the employment is at arm’s length)

- The benefit must be offered to all employees in the same class

- Your personal benefit is capped at $1,500 per year (or $750 if you don’t have dependents)

These limits make PHSPs significantly less valuable for unincorporated businesses. If you’re a sole proprietor spending $5,000+ per year on medical expenses, this is one of the stronger arguments for incorporating. The PHSP savings alone can justify the cost of incorporation and annual corporate filing.

What Expenses Are Covered by a PHSP?

A PHSP covers any expense that qualifies as an eligible medical expense under section 118.2(2) of the Income Tax Act. This is the same list CRA uses for the Medical Expense Tax Credit (METC), but through a PHSP you get 100% coverage instead of a partial credit.

The list is broader than most people expect:

Commonly Claimed Expenses

| Category | Examples |

|---|---|

| Dental | Cleanings, fillings, crowns, root canals, orthodontics (braces), dentures, implants |

| Vision | Prescription glasses, contact lenses, laser eye surgery (LASIK, PRK), eye exams |

| Prescriptions | All prescription medications (not over-the-counter unless prescribed) |

| Paramedical | Massage therapy, physiotherapy, chiropractic, acupuncture, naturopathic medicine, osteopathy |

| Mental health | Psychologist, registered counsellor, psychotherapist |

| Medical devices | Hearing aids, orthotics, wheelchairs, CPAP machines, insulin pumps |

| Hospital and medical | Hospital stays, ambulance, lab tests, diagnostic imaging |

| Travel medical | Travel health insurance premiums, emergency medical care abroad |

| Other | Fertility treatments (IVF), medical cannabis (with prescription), service animals, home modifications for disability |

What’s NOT Covered

- Over-the-counter medications (unless prescribed by a doctor)

- Cosmetic procedures that are purely elective (cosmetic surgery, teeth whitening)

- Gym memberships (these fall under Wellness Spending Accounts, which are a separate product)

- Health supplements and vitamins (unless prescribed)

For the complete and current list, CRA maintains the official reference at Eligible Medical Expenses. When in doubt, check here first, or ask your accountant.

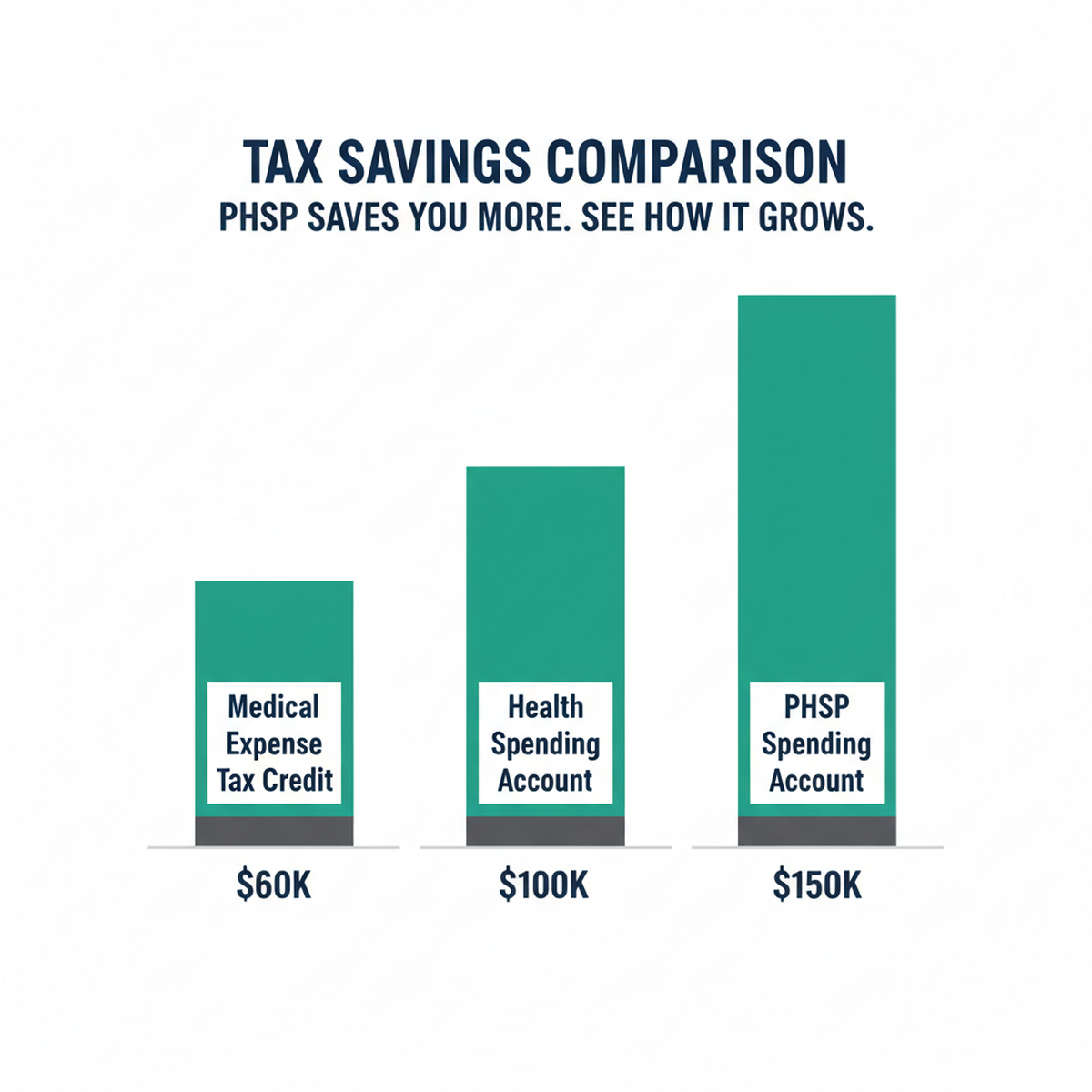

How Much Tax Will You Actually Save? (Real Numbers)

This is where most PHSP content falls short. Everyone says “you’ll save money.” Here’s what that actually looks like at different income levels and provinces.

How the Tax Savings Work

Without a PHSP, you can claim medical expenses through the Medical Expense Tax Credit (METC) on your personal tax return. But the METC has a threshold: you can only claim expenses that exceed the lesser of 3% of your net income or $2,635 (2026 indexed amount). And even then, it’s a non-refundable credit at the lowest federal rate (15%), plus your provincial rate. You don’t get the full amount back.

With a PHSP, your corporation deducts the full expense. There’s no threshold. The savings equal your combined corporate and personal marginal tax rate on every dollar of medical expense, minus the small admin fee.

Tax Savings Comparison: PHSP vs. Paying Out of Pocket

Scenario: Family with $8,000 in annual medical expenses (dental, vision, prescriptions, therapy)

| Income Level | Province | PHSP Tax Savings | METC Savings | Net Advantage of PHSP |

|---|---|---|---|---|

| $60,000 | Ontario | $2,480 | $460 | +$2,020 |

| $60,000 | Alberta | $2,240 | $410 | +$1,830 |

| $60,000 | BC | $2,360 | $390 | +$1,970 |

| $100,000 | Ontario | $3,440 | $320 | +$3,120 |

| $100,000 | Alberta | $3,040 | $290 | +$2,750 |

| $100,000 | BC | $3,280 | $270 | +$3,010 |

| $150,000 | Ontario | $4,160 | $210 | +$3,950 |

| $150,000 | Alberta | $3,840 | $200 | +$3,640 |

| $150,000 | BC | $4,000 | $190 | +$3,810 |

The pattern is clear: the higher your income, the more a PHSP saves you. At lower incomes the METC gives you a modest credit. At higher incomes the METC threshold eats most of your claim, while the PHSP delivers full savings regardless.

What About the CPP Cost?

If you need to start paying yourself a salary to qualify for the PHSP (see the salary vs. dividend section above), you’ll owe CPP contributions on that salary (both the employee and employer portions). However, that salary also builds CPP retirement benefits and RRSP contribution room. Your accountant can model the full picture: PHSP tax savings vs. CPP cost vs. RRSP room generated, based on your specific numbers.

Quebec: A Special Case

In Quebec, PHSP benefits paid to shareholder-employees of closely held corporations may be treated as a taxable benefit for provincial tax purposes. The federal benefit remains tax-free, but Quebec’s Revenu can assess provincial tax on the benefit. If you’re a Quebec-based business owner, this doesn’t eliminate the PHSP advantage, but it reduces it. Work with your accountant to model the Quebec-specific numbers.

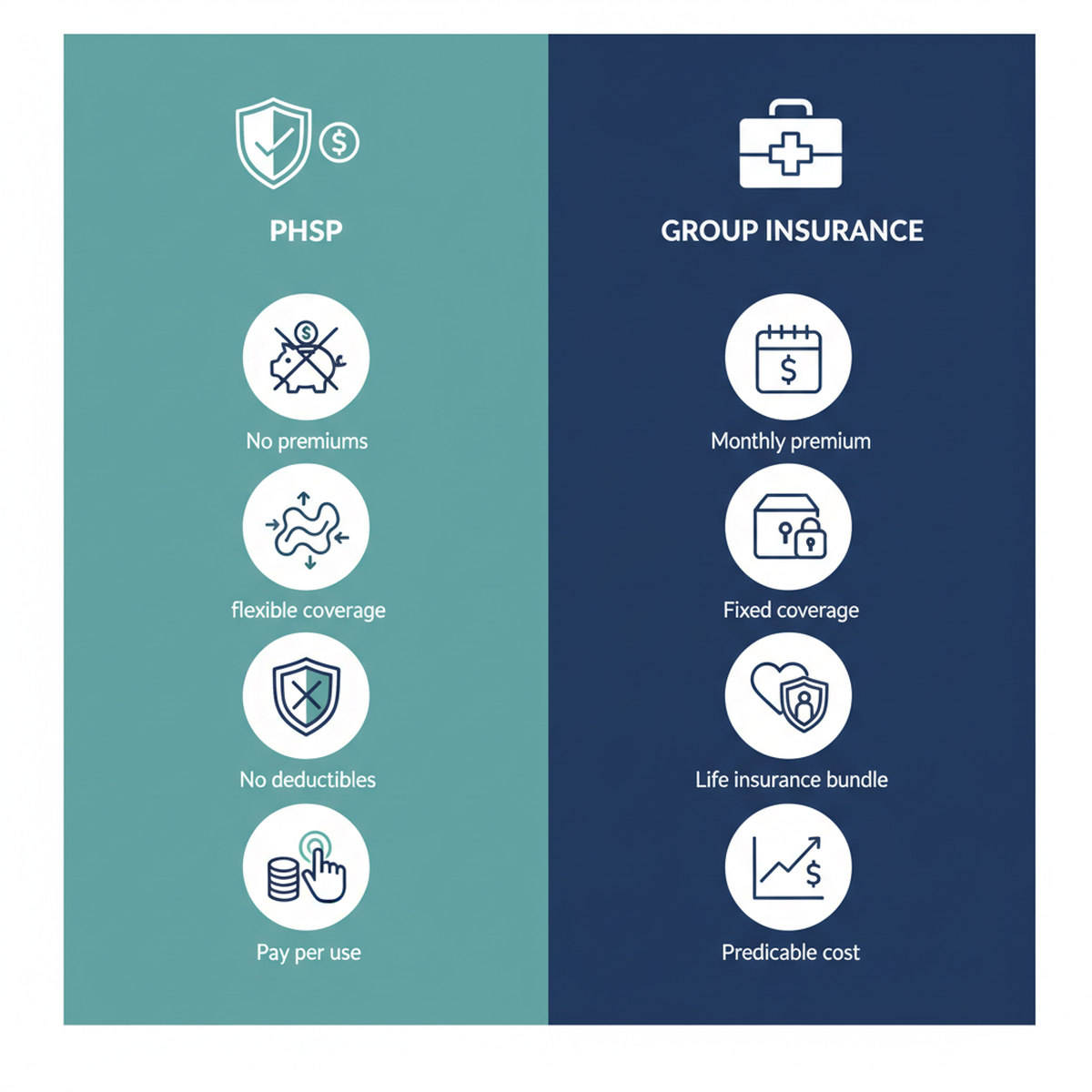

PHSP vs. Group Insurance: Which Is Better for Your Business?

This is one of the most common questions we get. The answer depends on your business size, your employees’ needs, and your budget.

| Feature | PHSP / Health Spending Account | Traditional Group Insurance |

|---|---|---|

| Monthly premiums | None. Pay only when claims are made | Yes. Fixed monthly per employee |

| Cost structure | Cost of claim + 5-10% admin fee | Premium + potential rate increases |

| Coverage flexibility | Any CRA-eligible medical expense | Limited to plan design |

| Deductibles / copays | None | Typically yes |

| Pre-existing conditions | No exclusions | May have waiting periods |

| Life / disability insurance | Not included | Often bundled |

| Best for | Small businesses, owner-operators, low-to-moderate claim volume | Larger teams wanting predictable costs, life/disability coverage |

When a PHSP Makes More Sense

- You’re a one-person corporation or have fewer than 5 employees. Group insurance minimum premiums often don’t make sense at this size. A PHSP gives you full coverage with zero fixed cost.

- Your medical expenses are moderate and predictable. If your family spends $3,000-$15,000 per year on medical expenses, a PHSP is almost always cheaper than group insurance.

- You want maximum flexibility. Group plans restrict which providers you can see and which drugs are covered. A PHSP covers anything on CRA’s eligible list.

- You’re healthy and don’t need life/disability. If catastrophic coverage isn’t a priority, a PHSP gives you exactly what you need with no extras.

When Group Insurance Makes More Sense

- You have 10+ employees and want predictable budgeting. Fixed premiums are easier to forecast than variable claims.

- Your team needs life insurance and long-term disability. A PHSP doesn’t cover these. Group plans bundle them.

- You have employees with high or unpredictable medical needs. Group insurance spreads risk across the pool. A PHSP means the corporation pays every dollar.

The Hybrid Approach

Many businesses use both. A basic group plan covers life insurance, disability, and a base level of drug and dental coverage, while a PHSP tops up anything the group plan doesn’t cover. This is increasingly popular with businesses in the 5-25 employee range.

HSA Limits and CRA Rules You Need to Know

For Incorporated Businesses

There is no fixed annual dollar limit on PHSP claims for incorporated businesses. CRA’s standard is that the benefit must be “reasonable.” In practice, this means:

- The benefit level should be proportional to the employee’s salary and role

- CRA may challenge claims that appear disproportionate relative to the salary being paid

- There’s no CRA bulletin with a hard dollar limit. “Reasonable” is assessed on the facts of each case

- Your accountant can help you determine what claim level is appropriate given your compensation structure

For Sole Proprietors

The limits are hard-coded:

- $1,500 per year per adult family member (you and your spouse)

- $750 per year per child

- Requires at least one arm’s-length employee enrolled in the plan

CRA Compliance Requirements

To keep your PHSP onside with CRA, you need:

- A written plan document. Your HSA provider will supply this. It outlines who’s covered, what’s eligible, and how claims are processed. Self-administered plans without formal documentation are a red flag.

- Third-party administration. CRA strongly prefers (and in practice requires) that a PHSP be administered by a qualified third-party administrator, not by the business owner themselves. Self-administered plans are technically possible but face much higher audit scrutiny.

- Legitimate employment relationship. T4 income for any owner-employee claiming benefits (see the salary section above).

- Consistent application. If you have multiple employees, the plan must be offered consistently within employee classes. You can have different benefit levels for different classes (e.g., management vs. staff), but you can’t offer a PHSP to yourself and exclude other employees in the same class.

- Proper receipts. Keep all medical receipts for a minimum of 6 years. Your HSA provider will retain copies, but keep your own as backup.

How to Set Up a PHSP for Your Business

Setting up an HSA takes about 15-30 minutes with most providers. Here’s the process:

Step 1: Choose a provider. Compare admin fees, setup costs, and features.

Step 2: Enroll and sign the plan agreement. The provider creates your plan document and sets up your account.

Step 3: Define your benefit classes. Decide who’s covered and at what level. For a one-person corporation, this is simple: one class, one member (plus dependents).

Step 4: Start claiming. When you incur an eligible expense, submit the receipt through your provider’s portal. They reimburse you and invoice your corporation.

Step 5: Your corporation deducts the full amount. The claim amount plus admin fee goes on your corporate tax return as a business expense.

What to Look for in a Provider

| Factor | What Matters |

|---|---|

| Admin fee | Typically 5-10% per claim. Lower is better, but check for hidden fees |

| Setup fee | Ranges from $0 to $335. One-time cost |

| Annual fee | Some charge $0, others $99-$249 per year |

| Claim turnaround | How fast you get reimbursed. Ranges from 24 hours to 7 days |

| Online portal | Can you submit claims digitally? Mobile app? |

| Plan document | Does the provider supply a CRA-compliant plan document? (They should) |

| Dependent coverage | Spouse and children included at no extra cost? (Standard) |

There are several reputable PHSP providers in Canada, each with different fee structures and features. We recommend researching multiple providers and comparing their setup fees, annual fees, per-claim admin fees, and claim turnaround times. Your accountant or financial advisor can help you evaluate which provider structure makes the most sense given your expected claim volume.

Common PHSP Mistakes to Avoid

We see these regularly in our practice. Each one can cost you the deduction or trigger CRA scrutiny.

Mistake 1: No Salary, Only Dividends

Already covered above, but it bears repeating. If you pay yourself zero salary and claim PHSP benefits, CRA can reclassify the benefit as a taxable shareholder benefit under section 15(1). Work with your accountant to determine the appropriate salary level to support your PHSP claims.

Mistake 2: Self-Administering Your Plan

Some business owners try to skip the provider and run the PHSP themselves to save the 5-10% admin fee. CRA has issued warnings about this. A self-administered plan without proper documentation, third-party oversight, and arm’s-length processing is very likely to be reassessed. The admin fee is the cost of compliance. Pay it.

Mistake 3: Claiming Ineligible Expenses

Gym memberships, supplements, cosmetic procedures, and over-the-counter products are not eligible. If these show up in your PHSP claims, the entire plan’s credibility is weakened. Your provider should catch these, which is another reason to use a reputable third-party administrator.

Mistake 4: Disproportionate Benefits

If your corporation has three employees but only the owner-shareholder uses the PHSP (and at a much higher level), CRA may challenge whether the plan is genuinely an employee benefit or a shareholder extraction scheme. The plan must be offered consistently within employee classes.

Mistake 5: No Written Plan Document

Every legitimate PHSP requires a formal plan document. This isn’t optional. It defines the classes of employees, the benefit levels, the eligible expenses, and the administration procedures. Your provider creates this. If you don’t have one, you don’t have a PHSP. You have an informal arrangement that CRA will disallow.

Mistake 6: Ignoring Quebec Rules

As noted above, Quebec may tax PHSP benefits at the provincial level for shareholder-employees of closely held corporations. If you’re in Quebec, make sure your tax planning accounts for this.

When a PHSP Does NOT Make Sense

We’re accountants, not PHSP salespeople. Here’s when we tell clients to skip it:

Your medical expenses are minimal. If your family spends less than $1,500 per year on medical, the admin fees and salary adjustment may not justify the setup. Run the numbers first.

You’re an unincorporated sole proprietor with no employees. The $1,500 annual cap and arm’s-length employee requirement make PHSPs impractical for most sole proprietors. Consider incorporating first, or use the METC on your personal return.

You need life insurance and disability coverage. A PHSP doesn’t provide these. If comprehensive risk coverage is your priority, a group benefits plan (possibly with an HSA top-up) is the better starting point.

You have highly unpredictable catastrophic medical expenses. A PHSP has no risk pooling. If someone in your family has $80,000 in annual medical costs, your corporation pays every dollar. Traditional insurance spreads that risk. For catastrophic scenarios, insurance is designed to do what a PHSP cannot.

You’re already getting full coverage from a spouse’s employer plan. If your spouse has a group benefits plan that covers your family, a PHSP only makes sense for expenses that plan doesn’t cover. It’s worth checking what falls through the gaps (orthodontics, paramedical visits above the group plan cap) before dismissing it.

How a PHSP Fits Into Your Overall Tax Plan

A PHSP doesn’t exist in isolation. It’s one piece of your tax and compensation strategy. Here’s how it connects to the bigger picture:

Salary vs. Dividends. As we’ve discussed, you need some T4 salary to support a PHSP. This changes the optimal salary/dividend split. Your accountant should model the combined effect: PHSP savings, CPP cost, RRSP room generated, and personal tax on the salary portion.

RRSP Contribution Room. The salary you pay yourself to support the PHSP also creates RRSP contribution room (18% of earned income). Depending on the salary amount, this can be a meaningful side benefit that adds up over time.

Corporate Year-End Planning. PHSP claims are deductible in the corporate fiscal year they’re paid. If your corporation has a strong profit year and you want to reduce taxable income, accelerating medical expenses (scheduling dental work, ordering new glasses, stocking up on prescriptions) before year-end is a legitimate planning strategy.

Integration with Group Benefits. If you already have a group plan, a PHSP can cover the 20-30% copay on paramedical services, the difference between your plan’s glasses allowance and the actual cost, or expenses your group plan excludes entirely.

Personal Tax Credits. You cannot claim the METC on your personal return for expenses already reimbursed through a PHSP. It’s one or the other. The PHSP is almost always the better choice, but your accountant should confirm based on your specific numbers.

Frequently Asked Questions

What is a PHSP (Private Health Services Plan) in Canada?

A PHSP is a CRA-approved plan that allows a Canadian corporation to reimburse employees for eligible medical expenses. The cost is 100% tax-deductible for the corporation, and the benefit is 100% tax-free for the employee. It’s also called a Health Spending Account (HSA) or Health Care Spending Account (HCSA).

What is the difference between a PHSP, HSA, and HCSA?

Nothing. They are different names for the same thing. PHSP (Private Health Services Plan) is the CRA’s official term. HSA (Health Spending Account) and HCSA (Health Care Spending Account) are marketing terms used by providers. The tax treatment is identical.

Can I set up an HSA if I only pay myself dividends?

Technically, some providers will let you enroll. But CRA requires that PHSP recipients have a legitimate employment relationship with the corporation, which means T4 income. If you claim PHSP benefits without any salary, CRA can reclassify the benefit as a taxable shareholder benefit. Talk to your accountant about what salary level makes sense given your specific PHSP claims and overall compensation structure.

Do I need employees to set up a Health Spending Account?

No. If you’re incorporated, you can set up a PHSP as the sole employee of your corporation. Sole proprietors, however, do need at least one arm’s-length employee.

What expenses are covered by a PHSP?

Any expense that qualifies as an eligible medical expense under section 118.2(2) of the Income Tax Act. This includes dental, vision, prescriptions, paramedical services (massage, physio, chiropractic), mental health, medical devices, fertility treatments, and more. The full list is maintained on the CRA website.

Is there a maximum limit on Health Spending Account claims?

For incorporated businesses, there is no fixed dollar limit. CRA’s standard is that the benefit must be “reasonable” relative to the employee’s compensation and role. For sole proprietors, the limit is $1,500 per adult and $750 per child per year.

How is a Canadian HSA different from an American HSA?

Completely different structures. A U.S. HSA is a personal savings account with tax-deductible contributions, investment growth, and withdrawal for medical expenses. A Canadian HSA is an employer-funded benefit plan where the corporation pays expenses directly. There is no personal account balance, no investment component, and no individual contribution. The only similarity is the name.

Are PHSP benefits taxable income?

No. PHSP reimbursements are received tax-free at the federal level and in all provinces except potentially Quebec, where shareholder-employees of closely held corporations may owe provincial tax on the benefit.

Can I claim massage therapy through my HSA?

Yes. Massage therapy provided by a registered massage therapist (RMT) is an eligible medical expense. Some provinces require a doctor’s referral for the METC, but not for PHSP claims. Check with your provider.

How much does it cost to set up a Health Spending Account?

Setup fees range from $0 to $335 depending on the provider. Most charge no annual fee. The ongoing cost is an admin fee of 5-10% per claim. On a $5,000 annual claim, that’s $250-$500 in admin fees, which is itself tax-deductible to the corporation.

Can CRA audit my Health Spending Account?

Yes. CRA can review any business deduction, including PHSP claims. Common audit triggers include: no T4 salary for the claimant, self-administered plans without proper documentation, disproportionate benefits relative to compensation, and ineligible expenses. Using a reputable third-party administrator with a proper plan document significantly reduces your risk.

Is a PHSP better than claiming the Medical Expense Tax Credit?

In almost every case, yes. The METC only provides a partial credit (at the lowest tax bracket rate) on expenses exceeding 3% of your net income. A PHSP provides a full deduction at your corporation’s and personal marginal tax rates with no threshold. The higher your income, the bigger the gap in PHSP’s favour.

Next Steps: Is a PHSP Right for Your Business?

If you’re incorporated, paying yourself at least some salary, and spending more than $1,500 per year on medical expenses for your family, a PHSP is almost certainly worth exploring. The process takes less than 30 minutes, and the annual tax savings can be significant depending on your income and expense level.

If you’re not sure whether the numbers work in your situation, or you need to adjust your salary/dividend mix to accommodate a PHSP, that’s exactly the kind of planning we do at Jones & Cosman.

Jones & Cosman CPA makes no representations or warranties about the accuracy, completeness, or suitability of the information contained herein and accepts no liability for any loss or damage arising from its use.

Rob Cosman is a CPA at Jones & Cosman CPA, where the firm helps Canadian business owners with tax planning, advisory, and business strategy.

Related Articles

- Can you pay your kids from your business in Canada?

- Should You Incorporate as A Canadian Amazon Seller?

- Claiming Home Expenses as Business Expenses

Related guides

Get the tax side right the first time.

We work with e-commerce and owner-managed businesses across Canada and beyond: GST/HST and provincial sales tax, corporate structure, income splitting, and non-resident compliance. Tell us your situation and we will tell you exactly what you need.

Get in touch