Should you buy a car through your corporation in Canada? If you spend any time on TikTok or Instagram, you’ve probably seen some financial “guru” telling you to buy everything through your company. Cars are the big one. And the advice sounds amazing in a 60-second clip. But the math almost never works the way these creators say it does.

Here’s what frustrates me. The number of people who just go ahead and buy a car in the company without talking to their accountant first is staggering. They show up at tax time with the car already purchased, already on the books, and then I have to explain why their personal tax bill just went up by thousands of dollars. Just ask first. One conversation before you sign at the dealership can save you a massive headache.

I see it constantly. Someone walks in excited because they watched a video about buying a G-Wagon through their business. Ten minutes into the conversation, after we run the actual numbers, the excitement disappears.

Last updated: April 2026

The TikTok Tax Advice Problem

These are real claims getting millions of views:

- “Buy a car in your LLC and write it off!” LLCs don’t exist in Canada. We have corporations, sole proprietorships, and partnerships. This is American advice that doesn’t apply here at all.

- “If the vehicle weighs over 6,000 lbs, you can expense the whole thing!” That’s the US Section 179 deduction. Canada doesn’t have anything like it. Our CCA (Capital Cost Allowance) system works completely differently.

- “Just put your logo on the car and write off 100%!” Slapping a decal on your BMW doesn’t make your personal driving tax deductible. CRA looks at actual usage, not branding.

- “Your corporation pays for the car so you save on taxes!” This ignores the standby charge, a taxable benefit that gets added to your personal income. You often end up paying MORE tax, not less.

Here’s the thing that really gets me. Anyone can call themselves a “financial guru” or “tax expert” online. There’s no barrier. Meanwhile, CPAs go through years of education, exams, and professional standards just to earn the designation, and we can’t even call ourselves “gurus” in good conscience. These creators have no accountability when their advice blows up in your face. Your accountant does.

Most of them are American, giving US tax advice to a global audience. The rules here are fundamentally different, and following their advice can cost you thousands in unexpected taxes.

How It Actually Works in Canada

When your corporation owns or leases a vehicle that you use personally (even a little), CRA requires two taxable benefits added to your income:

1. The Standby Charge

This one catches people off guard. The standby charge is based on the cost of the vehicle, and it’s charged for every month the car is available to you for personal use. Not every month you drive it personally. Every month it’s available. Car sitting in your driveway on a Saturday? CRA considers that available for personal use.

Company-owned vehicle:

- 2% of the original cost including GST/HST and PST, per month

- That’s 24% of the total tax-included cost, every year, added straight to your taxable income

Company-leased vehicle:

- 2/3 of the monthly lease payment (including GST/HST), per month

2. The Operating Expense Benefit

On top of the standby charge, if the corporation pays for gas, insurance, maintenance, or any operating costs, CRA tacks on another taxable benefit:

- 2026 rate: $0.34 per personal kilometre driven

- Alternative: If your business use is over 50%, you can elect 50% of the standby charge instead (sometimes lower)

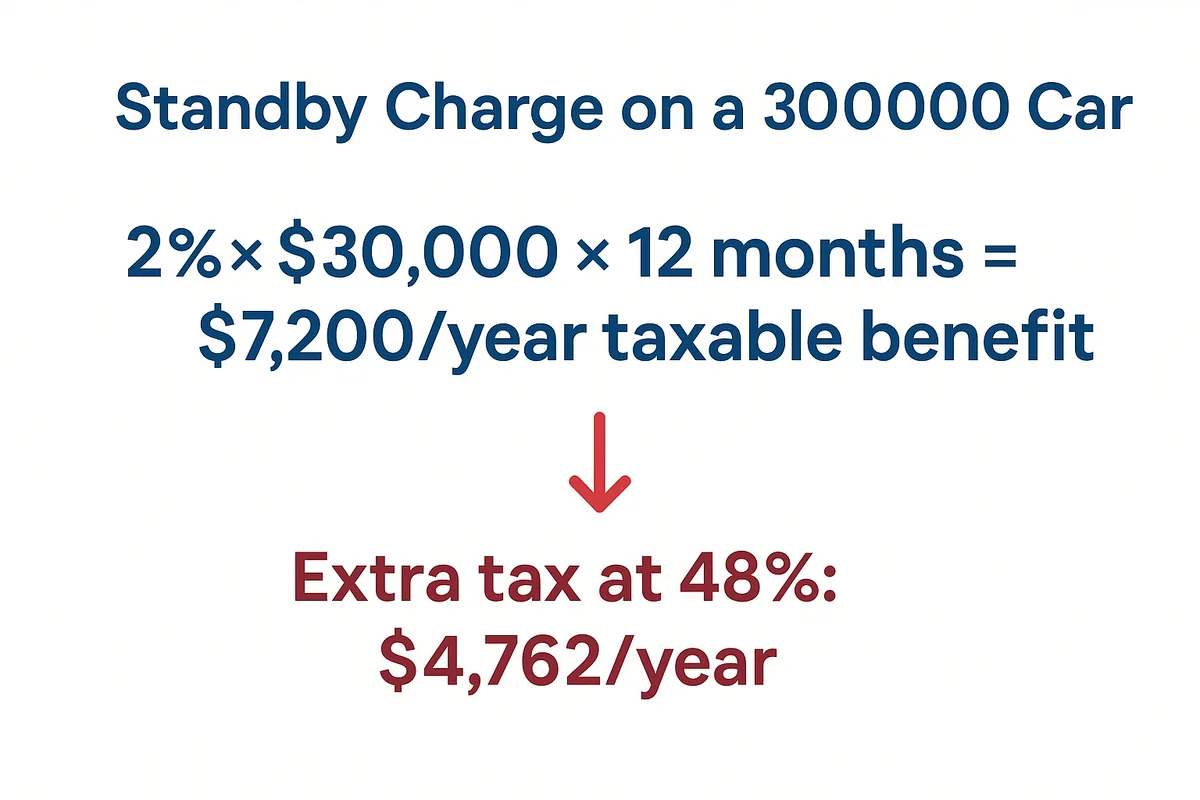

The Math: $30,000 Car Through Your Corporation

Let’s walk through what actually happens. This is the part your TikTok guru skips.

Scenario: $30,000 all-in price (including sales tax), 20,000 km/year, 60% business / 40% personal

| Calculation | Amount |

| Vehicle cost | $30,000 |

| Standby charge: 2% x $30,000 x 12 months | $7,200/year |

| Personal km: 20,000 x 40% | 8,000 km |

| Operating benefit: 8,000 km x $0.34 | $2,720/year |

| Total taxable benefit on your income | $9,920/year |

At a combined marginal tax rate of 48% (pretty common in most provinces once you’re over $100k):

Extra personal tax: $9,920 x 48% = $4,762 per year

That’s $4,762 in additional personal tax, every year, on top of what the corporation already spent on the car. Over five years you’re looking at nearly $24,000 in extra personal taxes. On a $30,000 car.

What About the Corporate Tax Savings?

Sure, the corporation gets to deduct car expenses. But those deductions are capped:

- CCA limit (2026): You can only depreciate up to $39,000 before tax for passenger vehicles (Class 10.1). Buy a $60,000 car? Too bad, you’re still only depreciating $39,000 of it.

- CCA rate: 30% declining balance. Not straight-line, so it takes years to fully depreciate.

- GST/HST ITC limit: Your input tax credit is capped at the GST/HST on $39,000.

- Lease cap (2026): $1,100/month before tax maximum.

- Interest cap (2026): $350/month maximum on vehicle loans.

The corporate deduction saves roughly 12-15% in corporate tax (small business rate). But you’re paying 48% personally on the taxable benefit. The numbers don’t work. You’re losing money.

Shareholder vs. Shareholder-Employee: This Matters

How you’re set up with the company changes things:

Shareholder-Employee (Most Common)

The standby charge and operating benefit show up on your T4 as employment income. CPP contributions may also apply on this amount. You pay full personal tax on the benefit.

Shareholder Only (Not on Payroll)

If you’re not an employee of the corporation and it provides you a vehicle, CRA treats the benefit under Section 15(1) of the Income Tax Act. You report it on a T4A slip, not a T4. And here’s what catches people: it’s not taxed as a dividend, so you don’t get the dividend tax credit. It’s included in your income at your full marginal rate. No gross-up, no credit, nothing to soften it.

The corporation can still deduct the car’s operating expenses and CCA on its side. But from your personal tax perspective, you’re paying full freight on the standby charge with zero dividend tax credit relief. I’ve seen business owners end up here because they never put themselves on payroll. It’s the most expensive way to handle it.

What We Actually Recommend: The Reimbursement Model

For most of our clients, here’s the approach that makes way more sense:

- You own the car personally

- You drive it for business and keep a mileage log

- The corporation reimburses you at the CRA prescribed rate

2026 CRA Prescribed Rates

- First 5,000 km: $0.73/km

- After 5,000 km: $0.67/km

- Territories: $0.77/km first 5,000, then $0.71/km

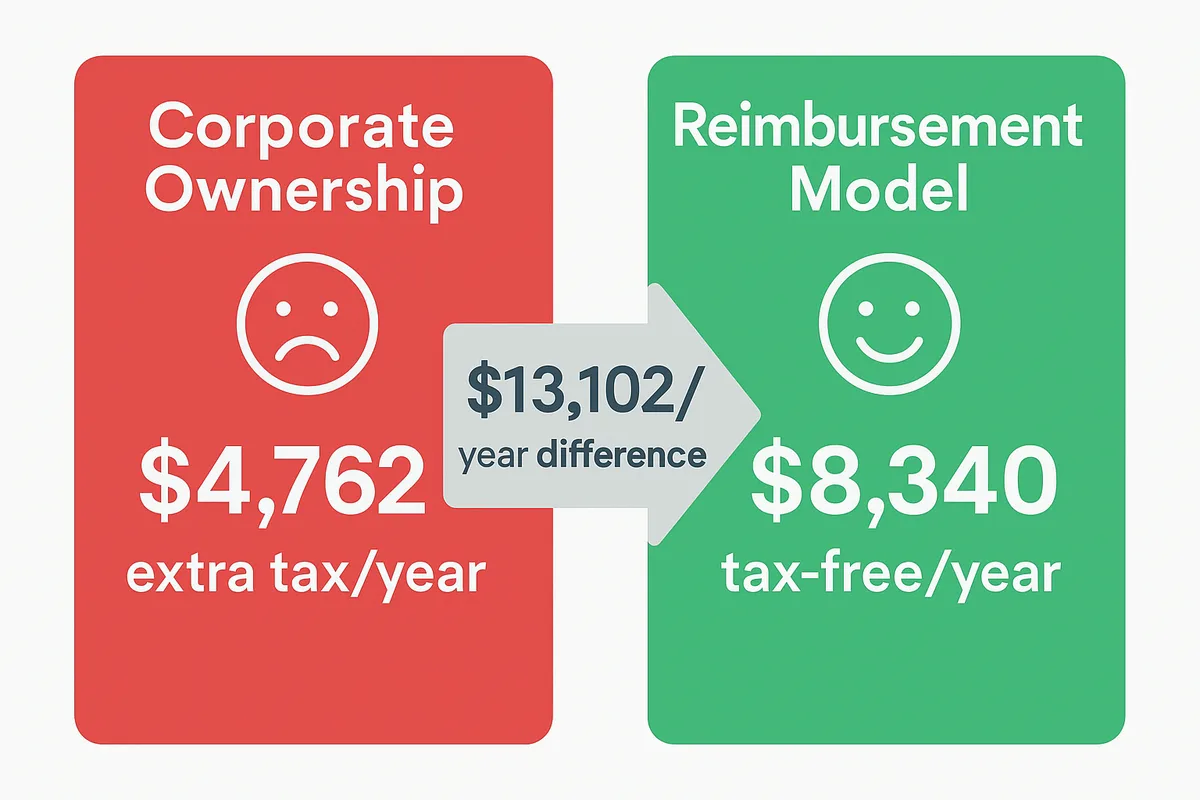

Same $30,000 Car, Reimbursement Model

| Calculation | Amount |

| Business km: 20,000 x 60% | 12,000 km |

| Reimbursement: 5,000 km x $0.73 + 7,000 km x $0.67 | $8,340/year |

| Personal tax on reimbursement | $0 (tax-free) |

| Corporate deduction | $8,340/year |

You get $8,340 per year, tax-free. The corporation deducts the full amount. No standby charge. No operating benefit. No surprise on your T4.

With corporate ownership, you paid $4,762 in extra tax. With reimbursement, you pocket $8,340. That’s a $13,102 per year swing. Same car. Different structure. Massive difference.

When Corporate Ownership Actually Makes Sense

It’s not always the wrong call. Here are the situations where it can work:

1. You Use the Vehicle 90%+ for Business

If you meet both conditions: business use over 50% AND personal driving under 1,667 km per month, the standby charge gets reduced proportionally using CRA’s formula. Think delivery vehicles, work trucks, or cars shared between multiple employees. For a vehicle at 95% business use, the standby charge practically disappears.

2. Commercial Vehicles

Pickup trucks over 6,700 lbs GVWR, cargo vans, and vehicles built for commercial use get classified differently. They may fall under Class 10 (no cost ceiling) instead of Class 10.1, so the full cost is depreciable. But the vehicle needs to actually be used for hauling and commercial work, not commuting.

3. Fleet Vehicles for Employees

If you’ve got sales reps, technicians, or delivery drivers who need vehicles, corporate ownership with proper tracking often beats reimbursing everyone individually. Insurance can also be cheaper on a fleet policy.

4. Zero-Emission Vehicles

The CCA ceiling for EVs (Class 54) is $61,000 before tax, well above the $39,000 for gas vehicles. Combined with provincial incentives, electric vehicles through a corporation can pencil out better. The standby charge still applies though.

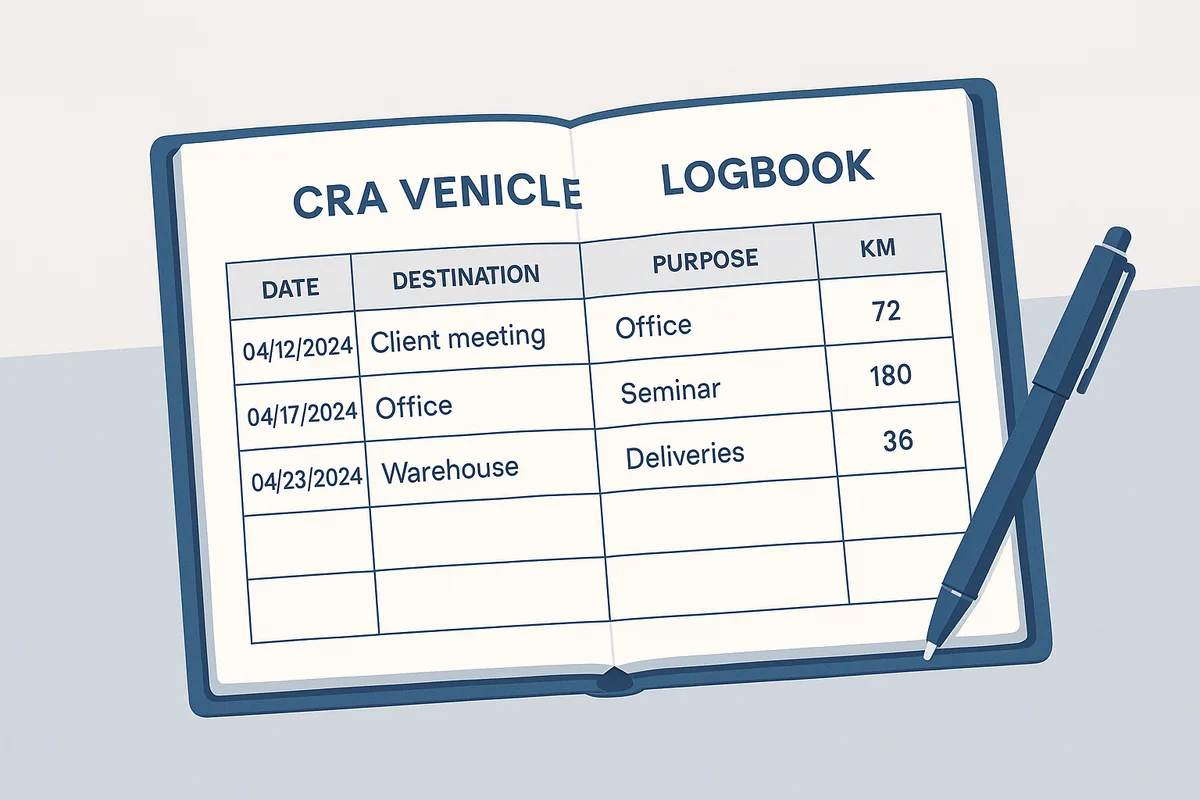

You Need a Logbook. Period.

Whichever model you use, CRA requires a vehicle logbook. This isn’t optional. It applies to:

- Corporate-owned vehicles (to prove the personal use percentage)

- Reimbursement claims (to verify your business kilometres)

- Sole proprietor vehicle expense claims

Record the date, where you went, why, and the kilometres. CRA says keep a full logbook for one complete year, then you can do a three-month sample in later years if usage stays consistent.

No logbook? CRA can deny everything or deem 100% personal use. I’ve seen it happen.

Frequently Asked Questions

Can I buy a car through my corporation in Canada?

You can, yes. But if you use it personally at all, CRA hits you with a standby charge (2% of cost per month) and an operating expense benefit on your personal taxes. For most owner-operators, this ends up costing more than it saves. Owning the car personally and taking the per-km reimbursement from your corporation is usually the better play.

What is the standby charge for a corporate vehicle in Canada?

It’s 2% of the original cost of the vehicle per month (24% per year) for purchased vehicles, or 2/3 of the monthly lease payment for leased ones. This goes on your personal taxes as a benefit. The charge can be reduced if you meet both tests: business use over 50% AND personal driving under 1,667 km per month.

Is the 6,000 lb vehicle write-off rule valid in Canada?

No. That’s US Section 179. It doesn’t exist here. In Canada, passenger vehicle depreciation is capped at $39,000 before tax (2026) no matter what the vehicle weighs. Heavy-duty commercial trucks may qualify for Class 10 with no ceiling, but standby charge rules still apply if there’s any personal use.

Should I incorporate just to buy a car?

No. Incorporation has real tax planning benefits, but buying a vehicle through a corporation is rarely one of them. The standby charge and operating benefit almost always create more personal tax than the corporate deduction saves. Please talk to your accountant before making this decision based on a TikTok video.

The Bottom Line

The “buy a car in your company” advice flooding social media is almost always American advice that doesn’t apply here, or Canadian advice that conveniently skips the standby charge math. When you actually run the numbers, most business owners come out ahead owning the car personally and taking the tax-free reimbursement.

Your situation might be different. Maybe you’ve got a commercial vehicle at 95% business use, or you’re running a fleet. Those are real scenarios where corporate ownership works. But for the typical business owner who drives to the office, runs some errands, and uses the car on weekends? The reimbursement model wins, and it’s not close.

Please, just ask before you buy. One conversation with your accountant before you sign at the dealership is all it takes. Don’t let a 60-second TikTok from someone with zero professional accountability make a decision that affects your taxes for the next five years.

Reach out if you want us to run the numbers for your specific situation.

Related guides

Get the tax side right the first time.

We work with e-commerce and owner-managed businesses across Canada and beyond: GST/HST and provincial sales tax, corporate structure, income splitting, and non-resident compliance. Tell us your situation and we will tell you exactly what you need.

Get in touch